Terminology Alignment: Gross Profit and Gross Margin

This article provides an explanation of frequently used terms to avoid confusion when discussing gross profit / gross margin and associated terms.

Gross Profit (GP)

- Refers to the Dollars (not a %) of profit

- Dollars a staffing firm gets to keep after paying the temporary workers payroll, benefits and payroll taxes (statutory expenses).

- Gross profit dollars are used to pay internal operating costs and owner's profit.

-

Actual Gross Profit = Revenue - COGS

- In Bullhorn terminology, GP = Billable Charge - COGS

- Note: Pay and Bill Adjustments will be incorporated into the calculation - see Adjustments definition for additional details

- Estimated Gross Profit = Revenue - (Payable Charges * (1 + Estimated Burden))

Gross Margin (GM)

- Refers to the Percentage of profit (not dollars)

- Percent a staffing firm gets to keep after paying the temporary workers payroll, benefits and payroll taxes (statutory expenses).

-

Actual Gross Margin = (Revenue - COGS) / Revenue

- In Bullhorn terminology, GM = (Billable Charge - COGS)/Billable Charge

- Estimated Gross Margin = (Revenue - (Payable Charges * (1 + Estimated Burden)))/Revenue

- Note: Pay and Bill Adjustments will be incorporated into the calculation - see Adjustments definition for additional details

Estimated Burden

- The estimated burden rate refers to the estimated costs to a company for hiring and maintaining a W2/T4 employee beyond their direct compensation in wages. Burden rates will include items such as training, fringe benefits, sick leave, and pension contributions, among several others.

- For Independent Contractors (ICs) and Subcontractors (SCs), since there are typically no costs associated with training, fringe benefits, sick leave, etc, the estimated burden would include costs to hiring and branch/AP support to process IC/SC payments. Therefore, the estimated burden for an IC/SC is significantly lower than for a W2/T4 employee.

- Estimated burdens are typically referenced as a percentage. (example 16% for a W2 or perhaps 4% for an IC).

-

Calculating a deal GM% using an estimated burden:

- GM = (Bill Rate - (Pay Rate * 1.16)) / Bill Rate

Actual Burden

- The actual burden rate consists of “actual” direct costs associated with employees, over and above gross compensation or payroll costs. Typical costs associated with the actual burden rate include payroll taxes, workers' compensation, company subsidized health insurance, paid time off, vacation, and sick leave, pension contributions, and other fringe benefits. Note: training and travel costs would only be included in the “actual” burden if these are processed through Payroll (rather than AP).

- From a perspective, actual burden incorporates Direct Labor Costs, which are processed through payroll.

- Due to the fact that the candidate costs that are paid through the client’s AP system are not fed into , these costs cannot be incorporated into the Actual Burden (i.e. drug/background tests, interview travel expenses, training expenses paid through AP, etc).

- For Independent Contractors (ICs) and Subcontractors (SCs), since there are typically no costs associated with training, fringe benefits, sick leave, etc, the burden would include costs to hiring and branch/AP support to process IC/SC payments. Therefore, the estimated burden for an IC/SC is significantly lower than for a W2/T4 employee.

-

Calculating weekly GM% using an actual burden:

- Weekly GM = (Weekly Billable $ - Weekly COGS) / Weekly Billable $

- Hourly GM% = Weekly GM/ # Hours Worked in that week

Direct Labor Costs (DLC) - aka Cost of Goods Sold (COGS)

-

All costs associated with a candidate’s payroll which include:

-

Payable Charge Items (Gross Pay):

- Pay for all hours worked (Reg, OT, DT, On Call, Call Back, etc)

- Pay for Bonus, PTO, Holiday, Sick Pay, Covid Pay

- Per Diem - taxed and non-taxed

- Non-billable expenses (i.e. moving reimbursement, interview travel reimbursement)

-

Employer Contributions from the Payroll Provider:

- Employer paid Social Security Taxes

- Employer paid Medicare

- Employer paid Unemployment Taxes

- Worker’s Compensation

- Employer paid retirement contribution

- Health insurance related expenses (ACA subsidies)

-

Payable Charge Items (Gross Pay):

can only capture Direct Labor Costs that are paid through Payroll. If the client needs to include candidate Direct Labor Costs that are paid through AP (i.e. pre-employment drug/background checks, interview costs, transportation and hotel expenses), since AP costs are not fed into Bullhorn One, the client would need to manage Direct Labor Costs through an external BI tool or the client’s accounting application.

-

These costs could fall into an Administrative Overhead category and would equate to additional burden above the DLC.

-

This functionality is not currently on the roadmap and would be future state (possibly 2023).

-

The intention would be “estimated” Admin Burden/Overhead and not actuals.

-

This could be a value add for clients that include Admin Burden as part of their Commissions calculations, but would be estimated and not actual.

Revenue for GP and GM Calculation

- In , Revenue refers to Total Billable Charge minus discounts, and not including taxes and passthrough billable expenses.

-

Billable expenses can be in two forms:

- Passthrough: the agency is passing 100% of the expense cost to the customer without any markup added.

- Markup: the agency is passing 100% of the expense cost to the

customer with a markup added.

- This markup is often considered an administrative markup since the Agency is performing administrative duties to validate and process the expenses.

- Although the Passthrough and Markup Billable Expenses would be considered “Revenue” on a P&L (profit and loss), for the calculation of GP and GM, these expenses are excluded from the revenue number.

- Revenue = Total Billable Charges - (Sales Taxes + Discounts + Billable Expenses)

- Discounts could include VMS fees, MSP fees, Tenure Discounts, etc.

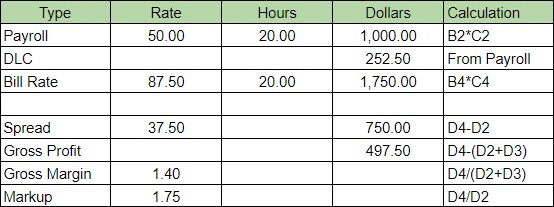

Spread

- Difference between the bill rate and the pay rate

- Does not include COGS or burden

- Spread = Bill Rate - Pay Rate

Markup

- A markup represents the percentage to be added to a pay rate to cover direct labor costs, operating expenses, and company profit.

- Markup % 's typically vary by industry vertical.

-

Example, if a staffing firm targets a 55% markup, the calculation would

be:

- Pay Rate * 1.55 = Bill Rate

Adjustments

-

Adjustments can be made to previous billable and payable charges and can

come in many forms:

- Bad Debt

- Correcting hours worked

- Retro correcting pay or bill rates

-

Write offs include:

- Revenue impacting write offs would be wrong rates, wrong hours, discounts, performance guarantees.

- The ones that impact Selling, General, and Administrative expenses (SG&A) are bad debt and recovery of bad debt

- Write offs are a type of financial adjustment that could impact Gross Profit and Gross Margin.

- Often write offs occur in a different time period than when the revenue and COGS were recognized, which adds complexity to calculating actual GM.

- provides clients

the ability to choose when to recognize the adjustments. When an

adjustment is entered and then exported to Payable Charges and/or

Billable Charges, the user will be prompted to enter the preferred

accounting date.

- Accounting Date: accounting period when the agency ties the

transaction to; determined by the agency on what date the agency

wants to associate the transactions as part of the agency’s GL.

- Agency wants to recognize the adjustment within the current week, then the agency user will enter the current week ending date as the “Accounting Date”.

- Agency wants to recognize the adjustment within the same time period when the initial transaction occurred, then the agency user will enter the applicable weekending date when the initial transaction occurred.

- Note: Accounting Date must be enabled as part of the agency setup.

- GP/GM Product reports will use the “Accounting Date” to incorporate adjustments into the GP/GM reporting.

- Accounting Date: accounting period when the agency ties the

transaction to; determined by the agency on what date the agency

wants to associate the transactions as part of the agency’s GL.

Terminology Alignment GP and GM - Sample Calculations

Permanent Placement Revenue

- For Permanent Placements, aka Direct Hire, the GP and GM terms do not typically apply. In contrast, common terminology associated with Perm Placements include:

- Dollar Fee - the dollar amount of the perm fee that will be invoiced to the client

-

Fee % - the corresponding Perm Placement fee percentage that will be

invoiced to the client. The % is typically applied to the candidate’s

hiring salary.

- Example, if the agency has a contractual agreement for a 20% perm placement fee, and the customer hires the candidate with a salary of $80,000, then the agency will invoice the customer for $16,000 ($80,000 * .20).

Any agency costs associated with the perm placement that are paid out of the agency’s Accounts Payable (AP) system will not be incorporated in the Bullhorn One reports. These costs could include:

-

Pre-employment drug/background screening

-

Sign on Bonus

-

Referral Bonus

-

3rd party payments to vendors to release a candidate from non-compete agreements.

Temp to Perm Revenue

- Many candidates start on a contract placement, and the client decides later to hire the candidate as a customer permanent employee.

-

In the Staffing Industry, this arrangement can be referred to using

various terms:

- Temp to Perm

- Contract to Perm

- Temp to Hire Conversion

- When a candidate is converted from a contractor to a permanent employee, there could be a fee that the agency would bill the client. This fee is similar to a Perm Placement fee; however, many agencies prefer to differentiate the Perm Placement fee from their Conversion fees on their P&L.

- Some agencies have customer contractual agreements that allow the customer to convert the candidate with zero fee.

Similar to the Perm Placement Revenue, reports related to Temp to Perm Revenue will not include any costs associated with the conversion if the costs are processed through the agency’s AP system, such as:

-

Sign On Bonus (if paid through Payroll while the candidate is on payroll, the cost will be associated with the contract assignment, rather than the conversion fee).

-

Bonus to help cover the cost of COBRA until the candidate is eligible for the customer’s insurance. (same situation as sign on bonus if paid through Payroll).

-

Pre-employment drug/background screening

-

3rd party payments to vendors to release a candidate from non-compete agreements.